Bad Credit? 5 Tips to Increase Credit Score (Do #1 Today!)

Bad credit in Fargo (or anywhere)? Looking to buy a house? Here are 5 tips to increase your credit score.

Fargo, ND has an unemployment rate roughly half of that of the national average. North Dakota in particular has the 5th best average credit score ranking in the US.

If you have bad credit in Fargo, it can make you feel like an outlier. If you’re looking to buy a house with bad credit, you might not have a great idea of just how much money your credit score is going to cost you over the length of your mortgage.

We’ve got you covered. First, we’re going to give you a rough idea of how much money you’ll save by improving your credit. After that, we’ll give you concrete, actionable tips that you can take to improve your credit score fast.

Good Credit Saves You Thousands of Dollars on Your Mortgage

A credit score is just an imaginary number that the bank uses to determine how risky it is to give you a loan, based on your repayment history for prior loans. So, you might be thinking, “Why do I even need a good credit score? What’s the point?”

Well, if you’re looking to buy a house, a good credit score could save you tens of thousands of dollars, because the bank uses that number to determine your interest rate. The riskier you appear to be, the more money they charge you. On the flip side, though, the safer you are (the higher your credit score), the less they charge you.

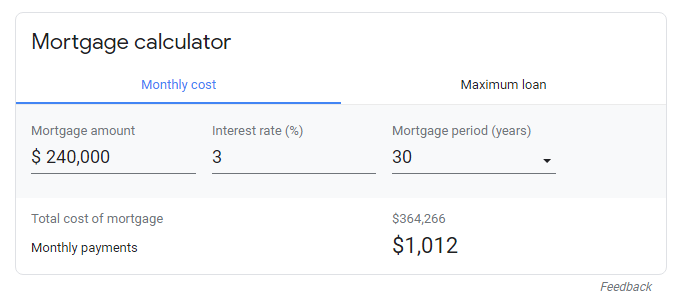

The average home value in Fargo right now is about $240k. With a good credit score (700-850), you could land a 3% interest rate. With a bad credit score, if you even qualify to buy a home, you’ll probably have a 5-6% interest rate.

Buying a Home in Fargo with Good Credit: The Numbers

We’re going to assume a 30-year fixed-rate mortgage. If you take out a $240k mortgage, with a 3% interest rate, your total payment will be $364,266 over 30 years.

Buying a Home in Fargo with Bad Credit: The Numbers

Meanwhile, if you take out a $240k mortgage with bad credit (a 5% interest rate), you’ll end up paying $463,814 over the course of the loan. That’s about $100k more than if you had a good credit score!

With that said, how can you get a good credit score?

Good Credit Tip #1: Pay Off Your Credit Cards Before the Payment Posts for the Month

When banks are looking at your creditworthiness, there are a few factors that make up their determination: payment history (35%), amounts owed (30%), length of credit history (15%), credit mix (10%), and new credit (10%).

The average student loan debt in the US is about $32,000. That makes up a huge chunk of the “amounts owed” factor.

But one thing that recent grads (and others) don’t realize is that you can pay off your credit cards before the bank issues a statement for that amount, lowering your total “amounts owed.” Instead of waiting for your monthly bill, just sign on and pay off your credit card, in full, before the bank sends you a statement.

The best thing about this tip is that you can do it today, and it can increase your credit score by 20-30 points over the next few months. It’s one of the easiest things you can do to quickly improve your credit.

Good Credit Tip #2: Make All Payments on Time

Payment history makes up the biggest chunk of your credit score.

This one should be obvious. Put yourself in the banks’ shoes: You wouldn’t want to lend money to someone who has a history of not paying it back, would you?

Whether it’s your car loan, student loan, or credit card, make all of your payments on time. If you’re having trouble making those payments because of a recent hit to your income, call up your lenders for those prospective loans and see if you can have the monthly amount reduced or postponed. This is typically much easier than you think, and it only requires a quick phone call.

Good Credit Tip #3: Keep Your Oldest Credit Card Open

Maybe you went through a period of credit card churning, when you opened new credit cards just to take advantage of the cash bonus and other rewards before closing it. Well, “length of credit history” is also an important factor, and it’s usually determined by the age of your oldest credit line and the average age of your open credit lines.

If you have a credit card that you opened a while ago that has a $0 annual fee, then, just keep it open and tucked away in a drawer.

Good Credit Tip #4: Mix Up Your Credit

“Credit mix” means that you’ve taken out lots of different loans and paid them off on time.

This is further down the list because it’s probably not something you have to consider. In fact, it’s probably something that happened naturally as you realized that you needed a credit card, a student loan, a car loan, and so on. Really, all you have to do is continue to pay those off.

In the event that you’ve never taken out a loan before, though, consider getting a credit card and paying it off in full every month to show the banks that you’re capable of managing your credit. If they don’t have any history to analyze, you could be the most responsible person on earth and you still wouldn’t have a credit score.

Good Credit Tip #5: Time

This is the least sexy of all the credit score tips. Whereas you can put #1 into effect immediately and see it work in fewer than a couple of months, the ultimate credit-building tip is time.

You just have to keep paying off your bills responsibly. It’s that simple (and that boring).

Conclusion: Bad Credit in Fargo? 5 Tips to Increase Your Credit Score (Do #1 Today!)

Having a bad credit score could cost you as much as $100k over the course of your loan in Fargo. There are a lot of things you could do to increase your credit score, and we listed some major tips here.

If you live in Fargo and have any questions about buying or selling a house with a bad credit score or a good credit score or anything in between, contact us and we’ll be happy to answer.